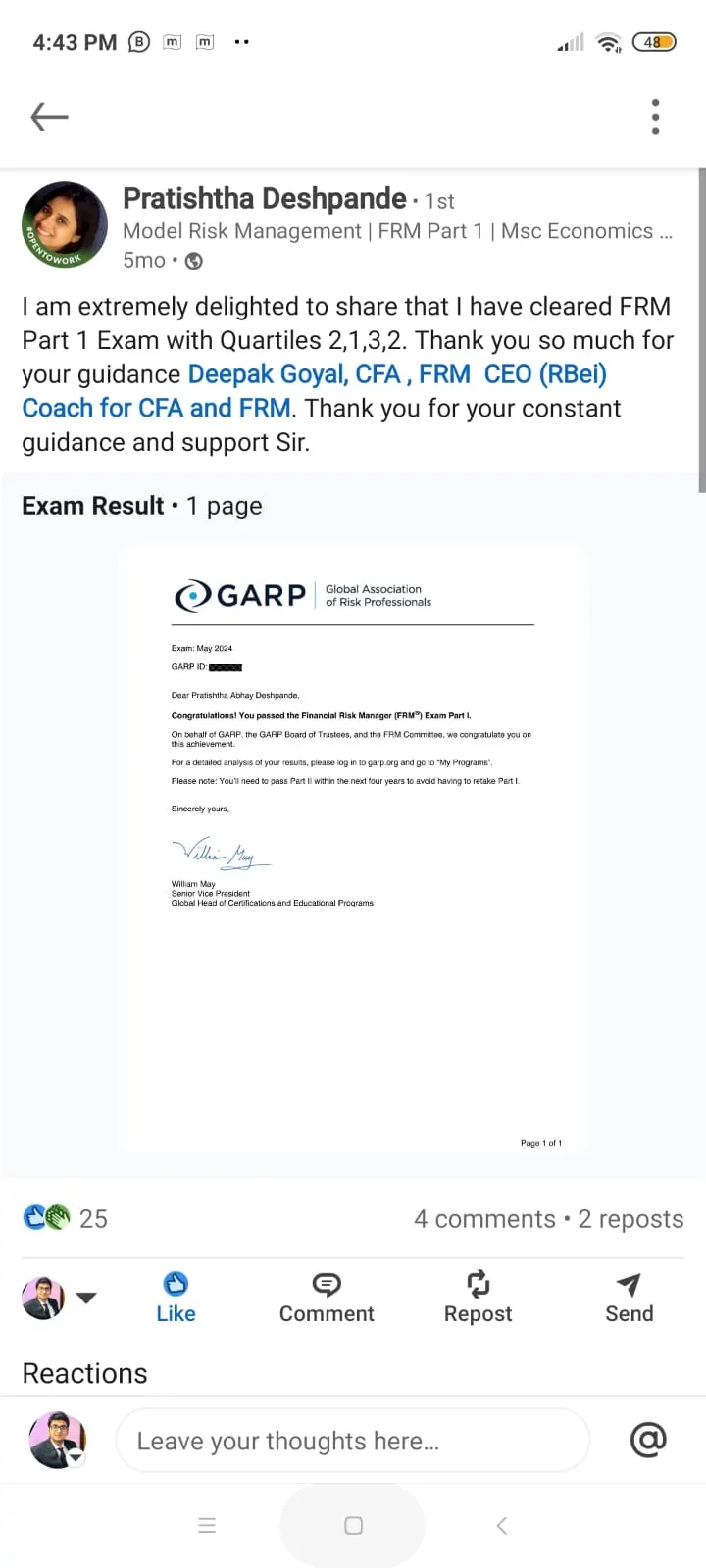

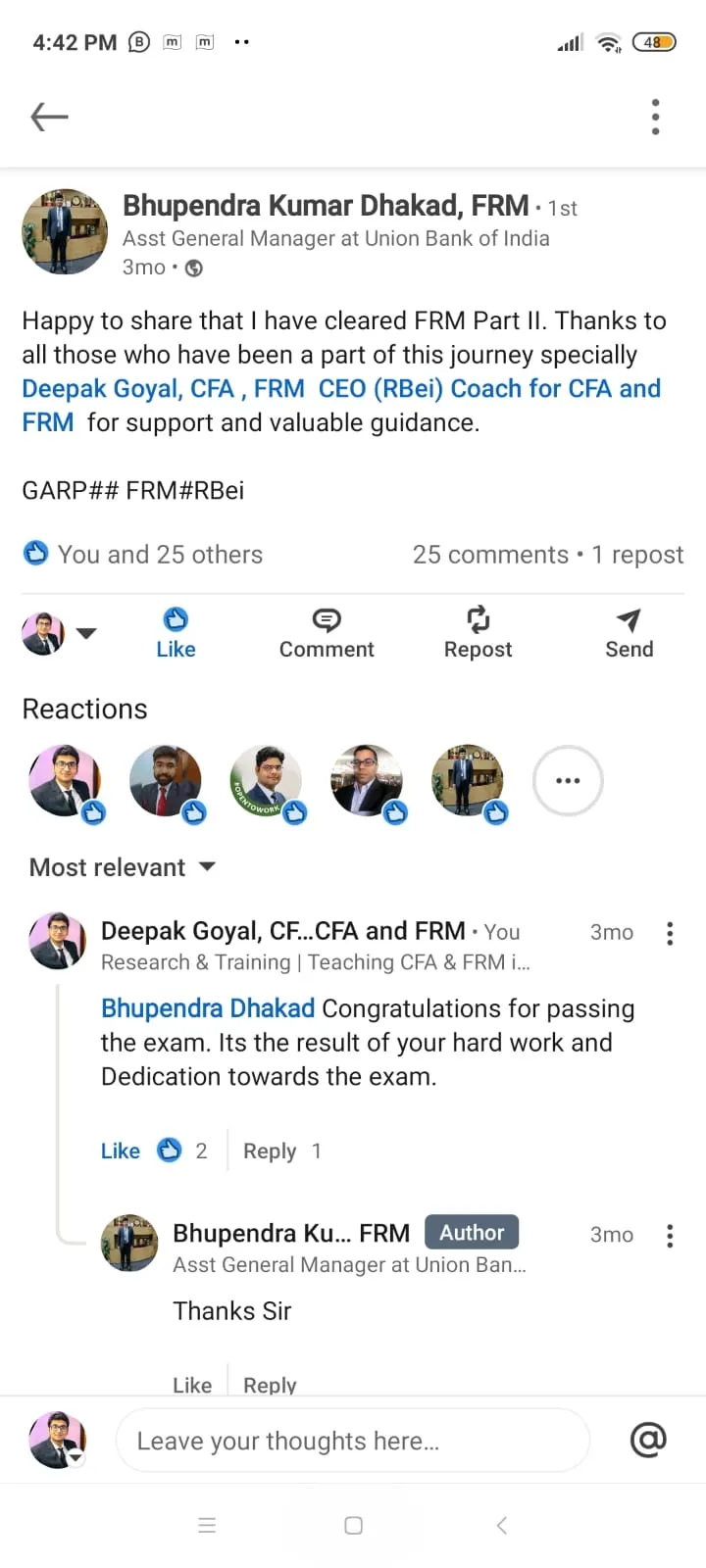

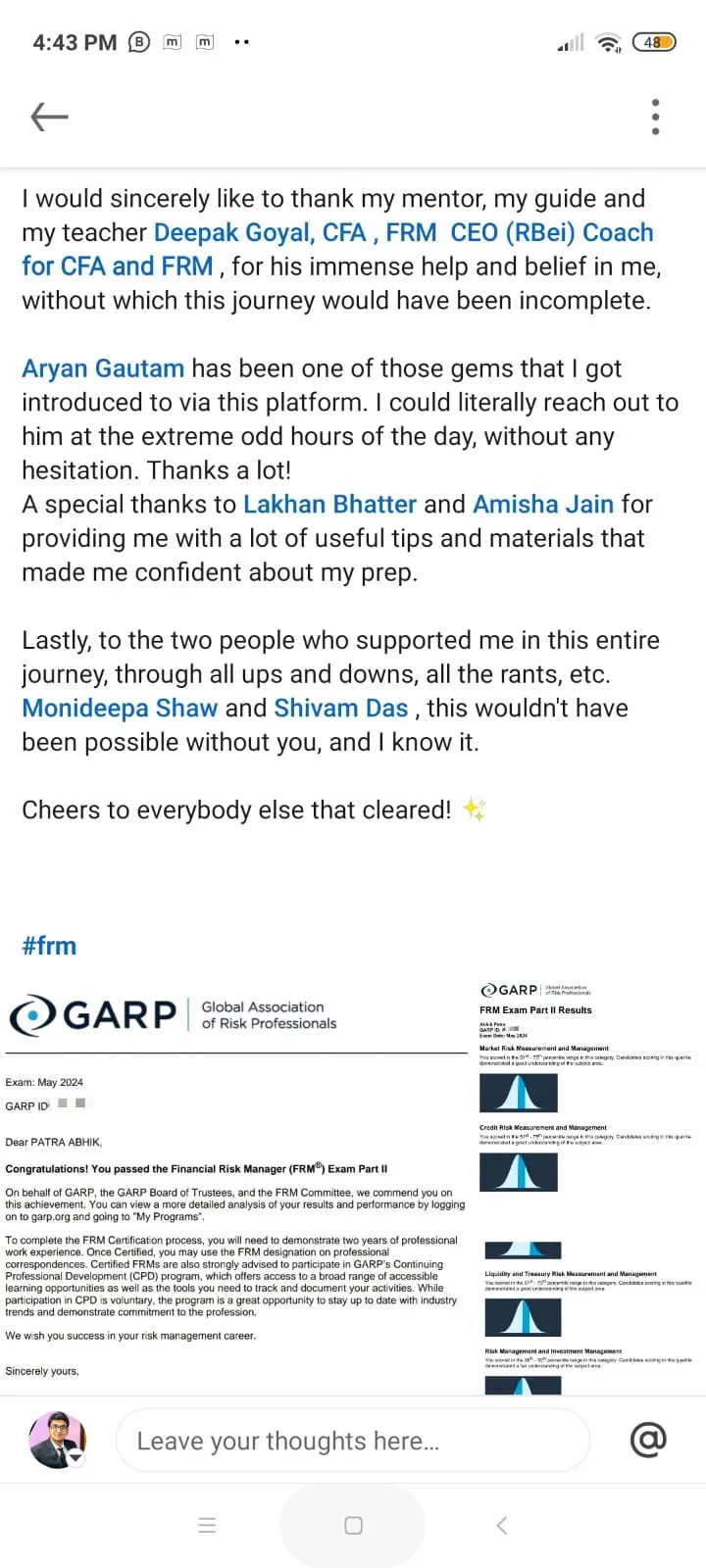

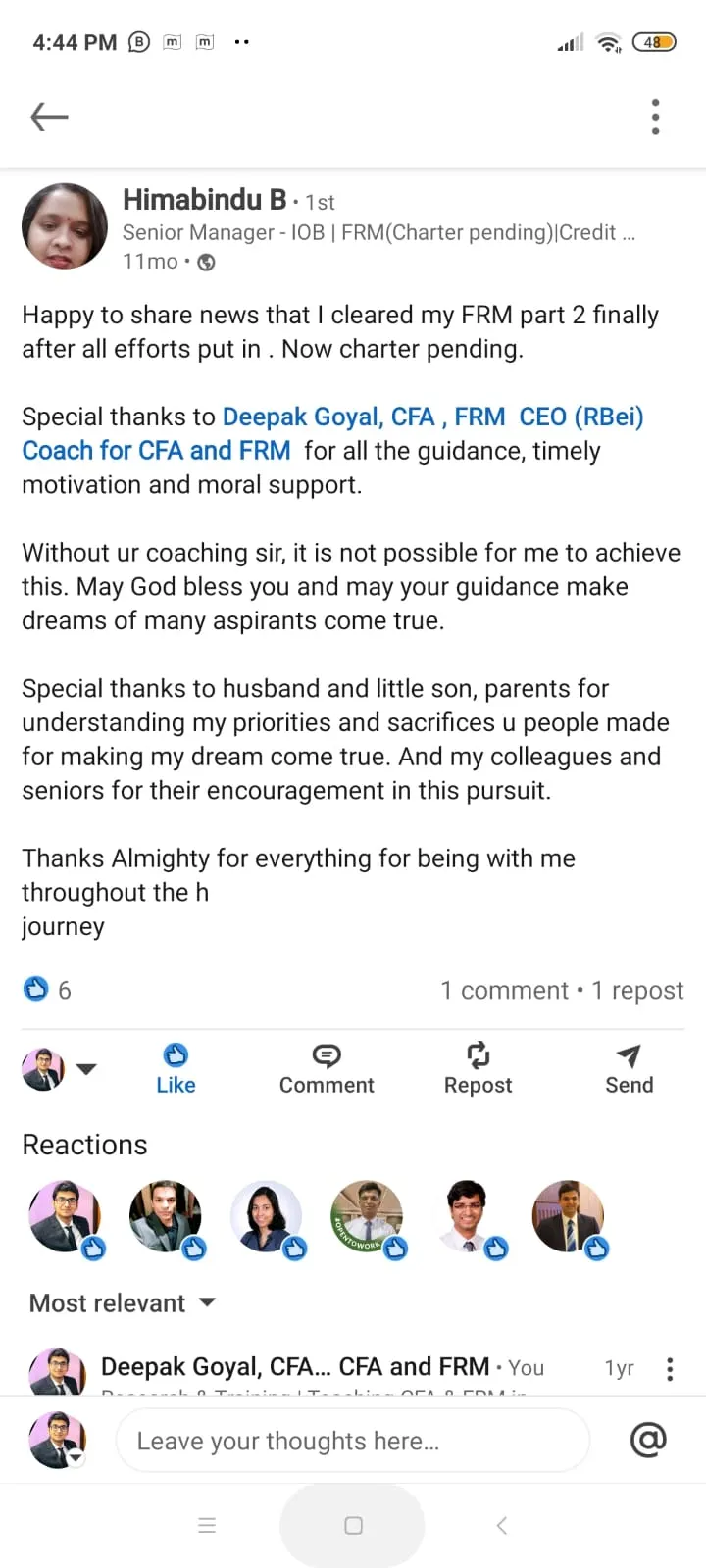

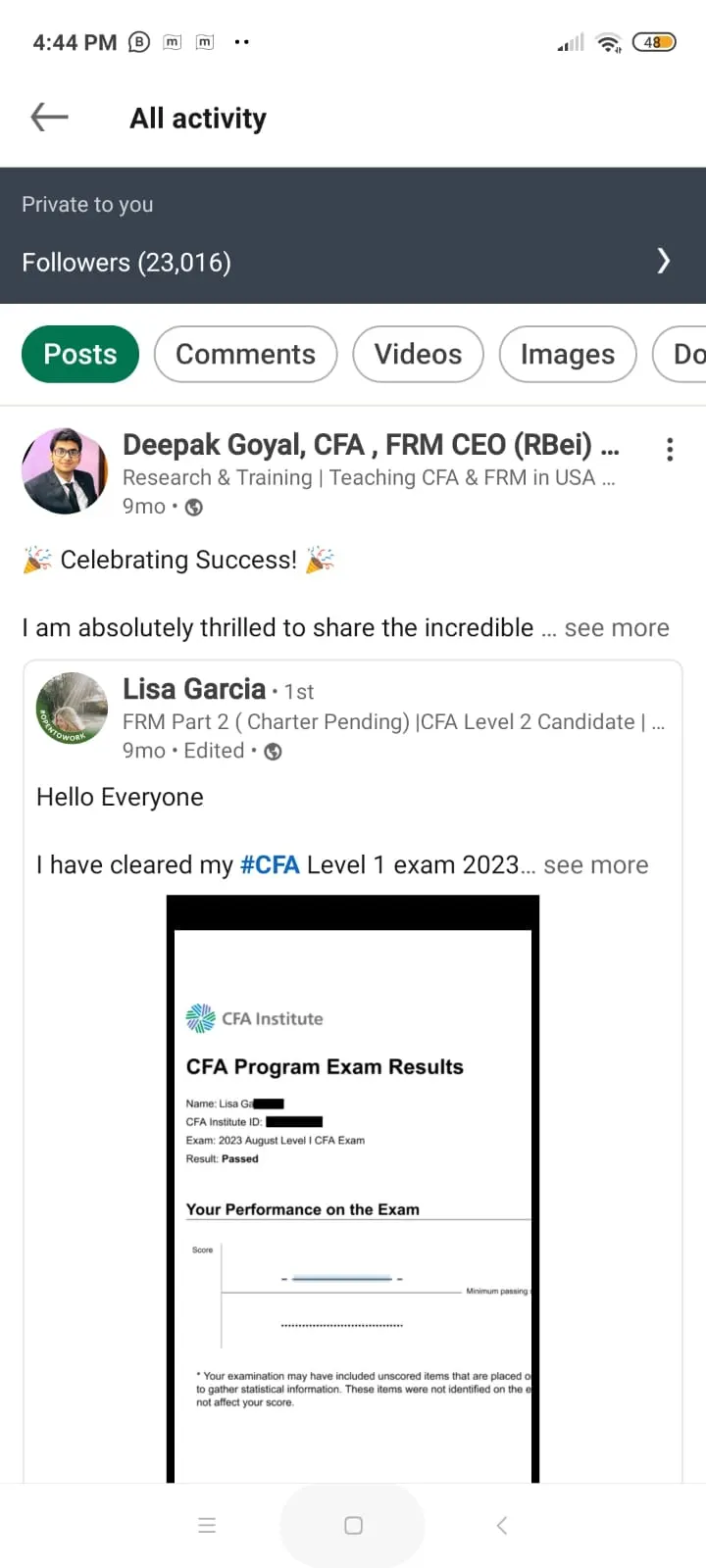

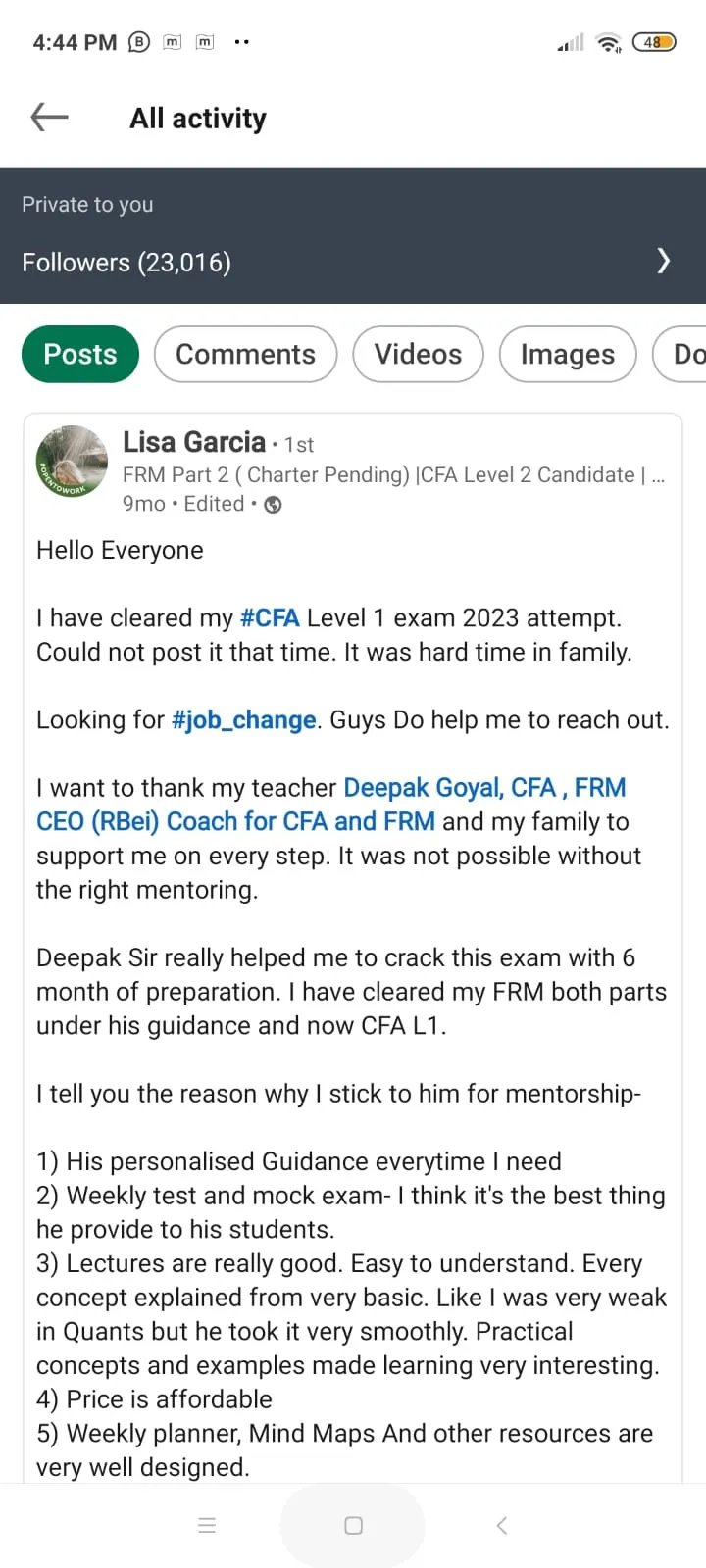

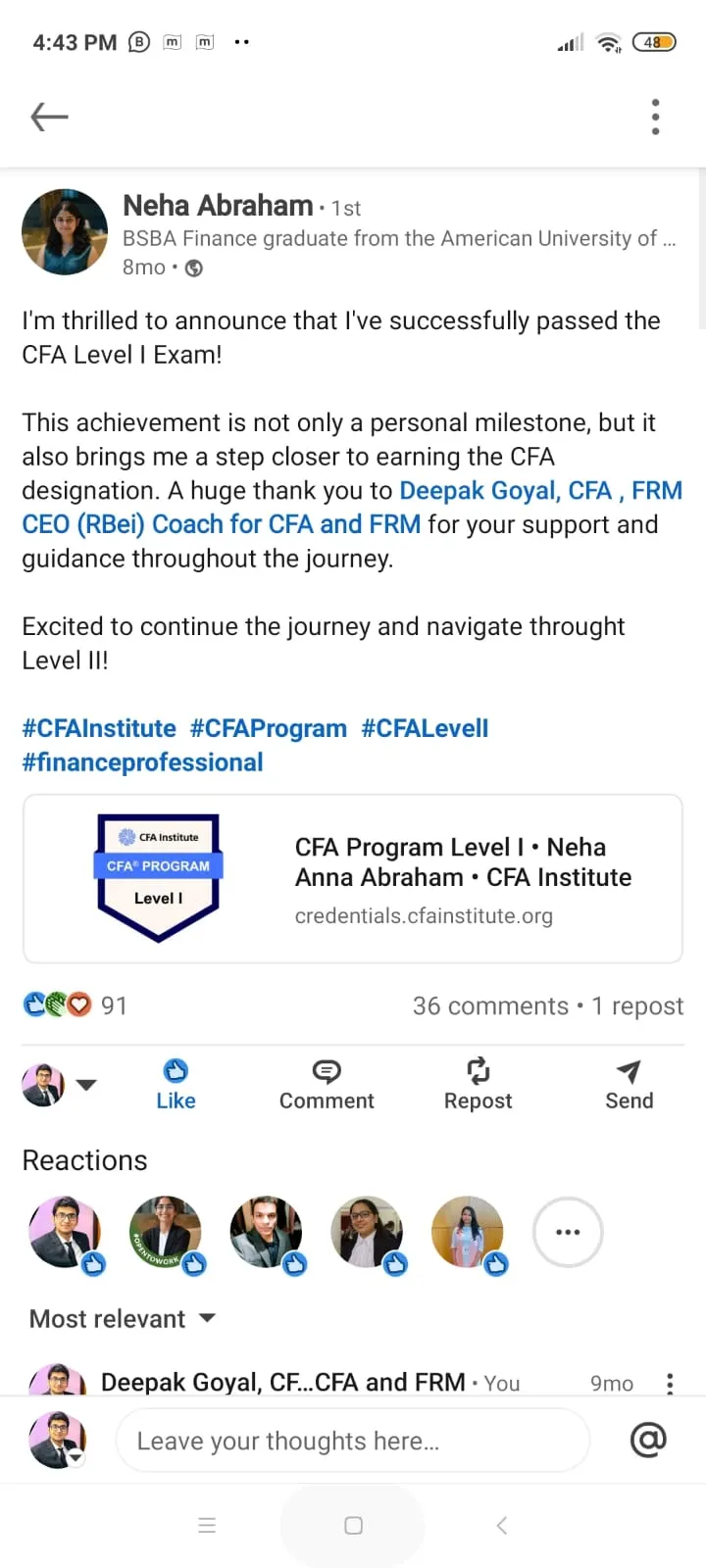

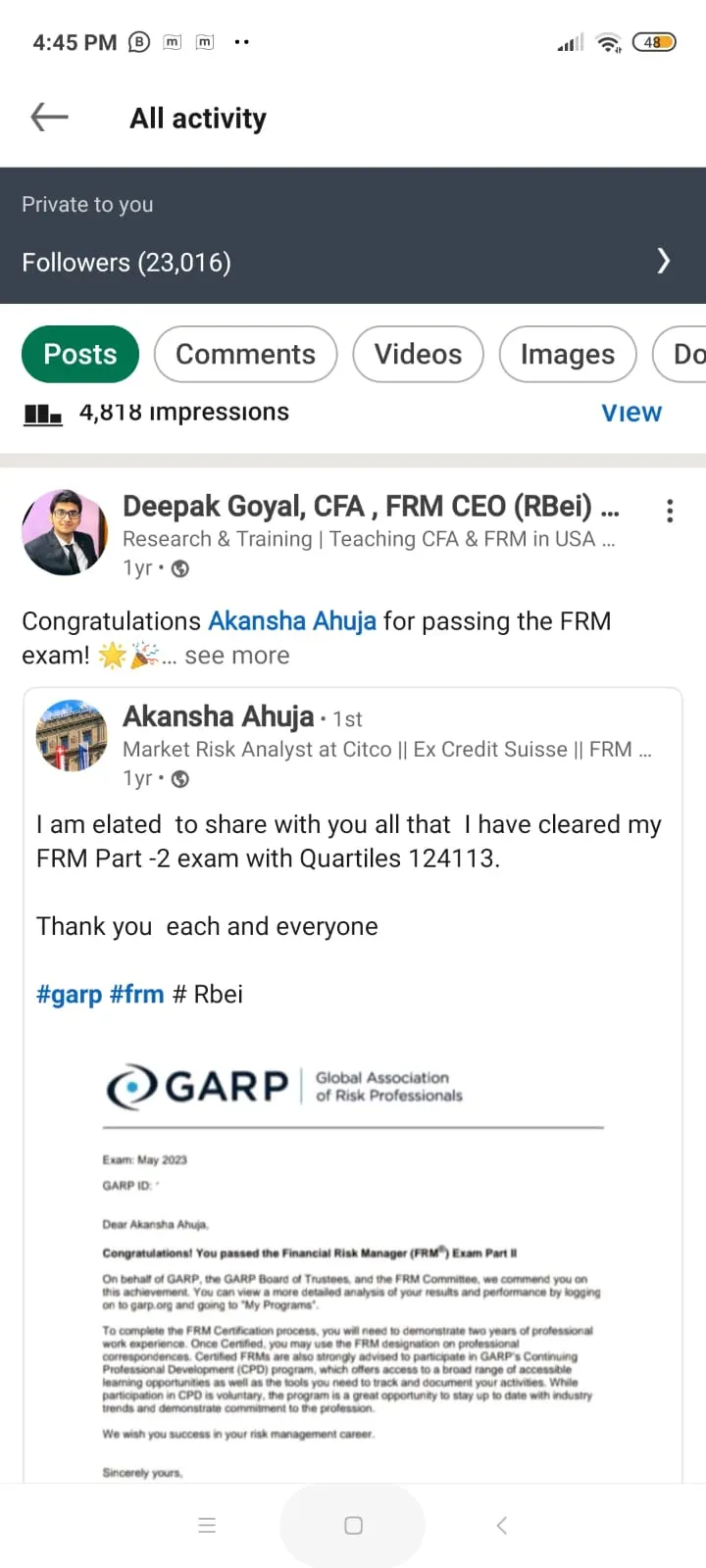

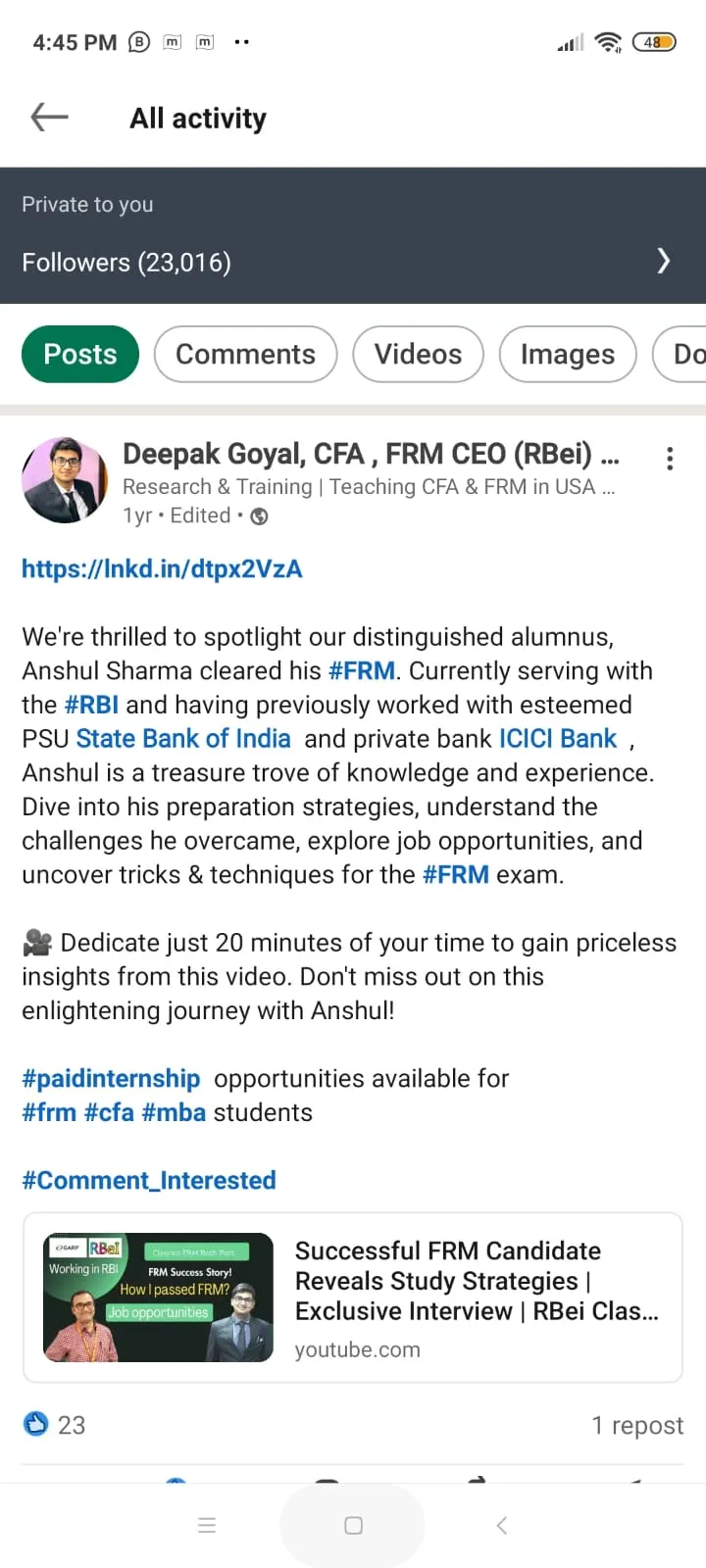

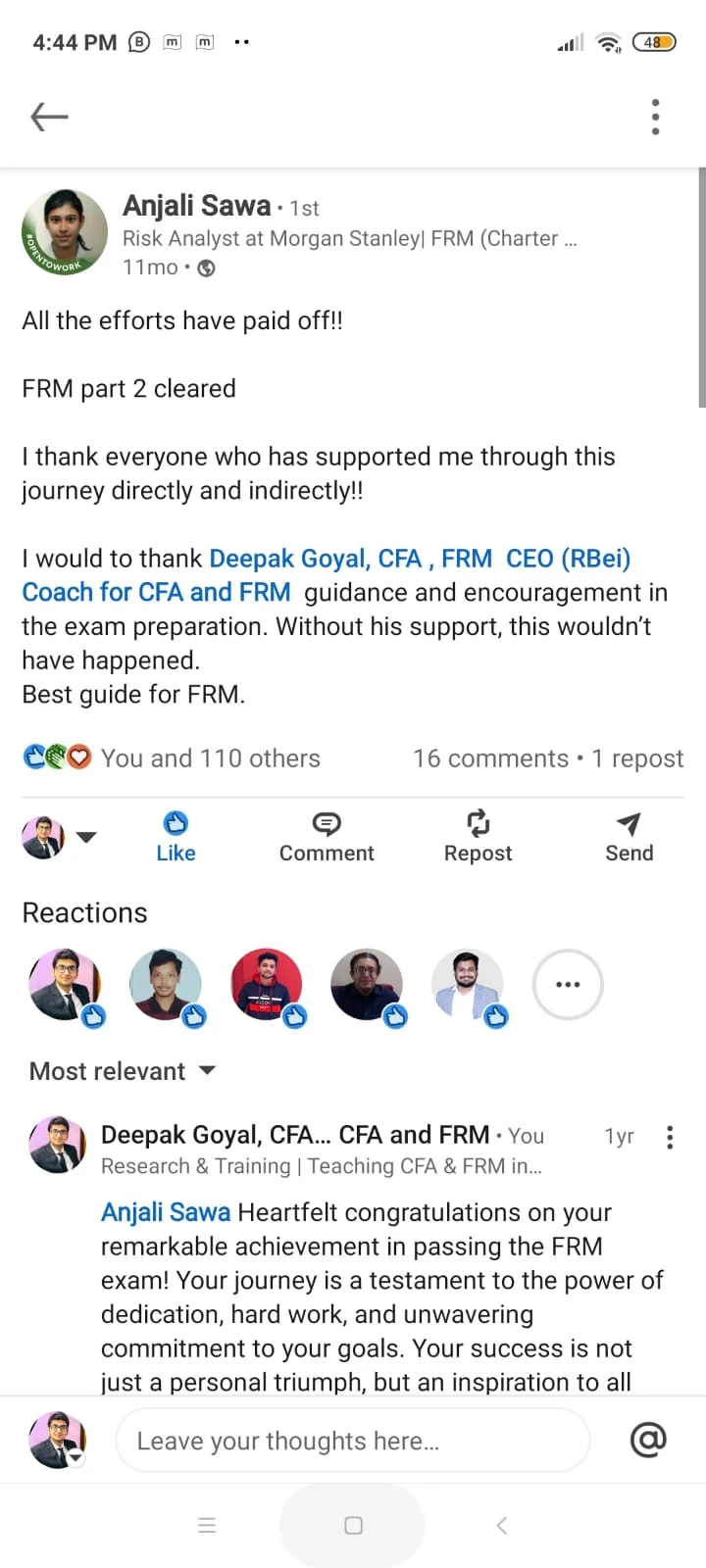

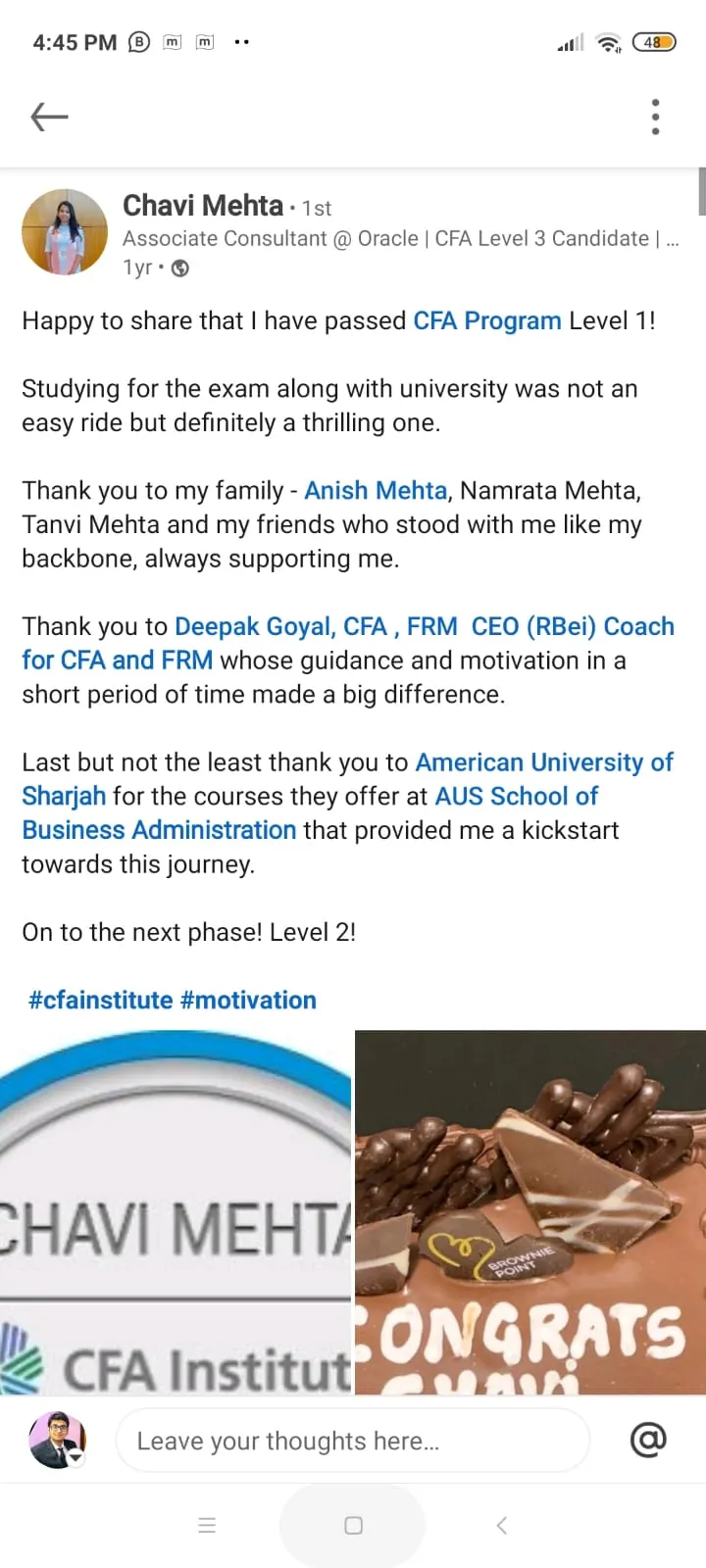

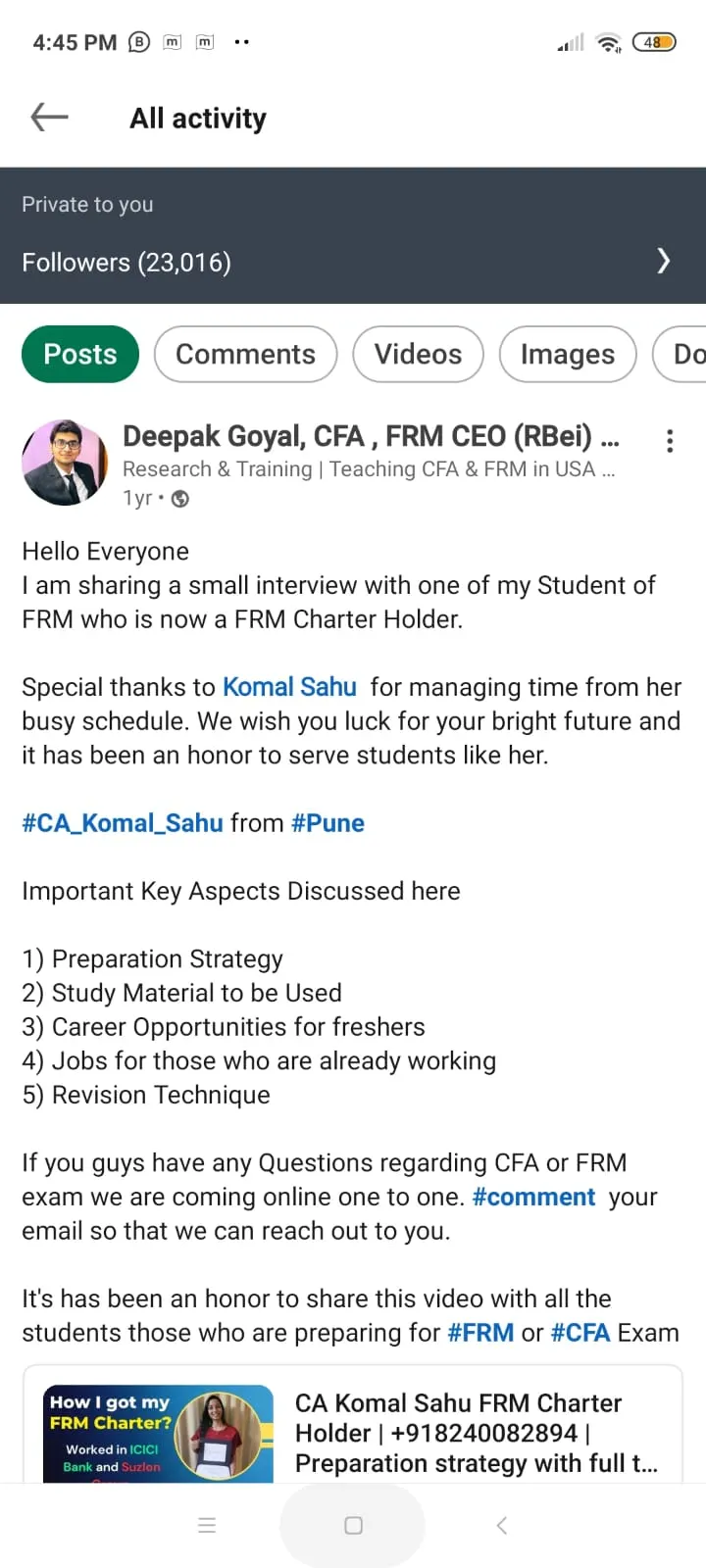

RBei Classes Student Success on LinkedIn

RBei Classes, an FRM & CFA coaching institute founded in 2018 by Deepak Goyal (CFA & FRM charterholder), has trained thousands of students who share their results publicly on LinkedIn. The 13 posts below are a sample of RBei Classes students announcing verified CFA and FRM passes — public, name-attributed proof of outcomes.

Key Takeaways

- RBei Classes students publicly share verified CFA and FRM results on LinkedIn, with name and profile attached.

- The 13 posts shown are a sample of the thousands of students trained by RBei Classes since 2018.

- Outcomes span CFA Level 1, CFA Level 2 prep, and FRM Part 1 & 2.

- Coaching is led by Deepak Goyal, CFA & FRM charterholder, founder of RBei Classes.

Last updated: June 2026 · Reviewed by: Deepak Goyal, CFA & FRM charterholder, founder of RBei Classes · Public LinkedIn posts shared by RBei Classes students.